One critical factor to consider when purchasing legal malpractice insurance is the insurance company’s financial strength. Since legal malpractice insurance (sometimes referred to as “long tail insurance”) often has claims that can take several years to resolve, it’s essential to choose an insurance carrier with strong long-term financial stability to ensure they can cover the expenses and damages associated with your claim.

What is a Financial Strength Rating?

Financial Strength Ratings show, as the name suggests, an insurance company’s financial strength but are indicators of the company’s ability to honor its obligations to their insureds.1 Independent rating companies such as A.M. Best and Standard & Poor’s provide reliable assessments of an insurance carrier’s financial strength and can help you make an informed decision about which carrier to trust with your legal malpractice coverage.

About A.M. Best

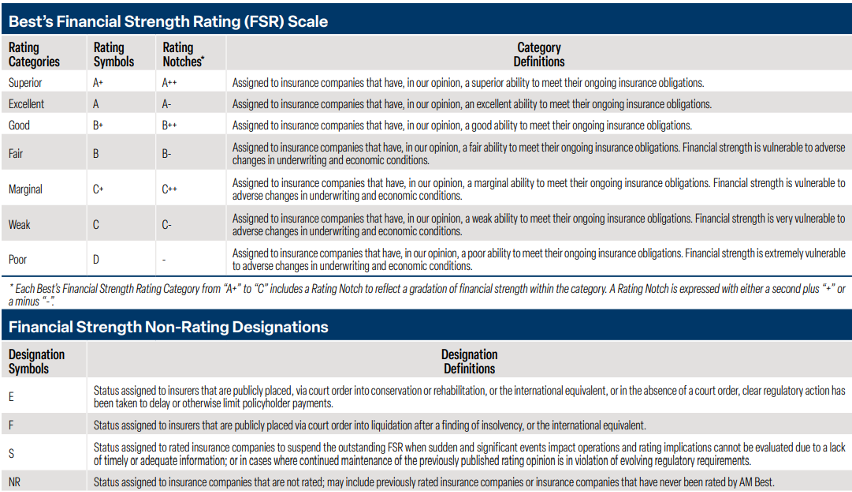

A.M. Best is the leading independent analyst of insurance companies, and they annually analyze the financial strength of insurance companies. A.M. Best awards its ratings in a range from A++ (Superior) to F (Insolvent).

This chart from the A.M. Best website explains their assigned ratings:

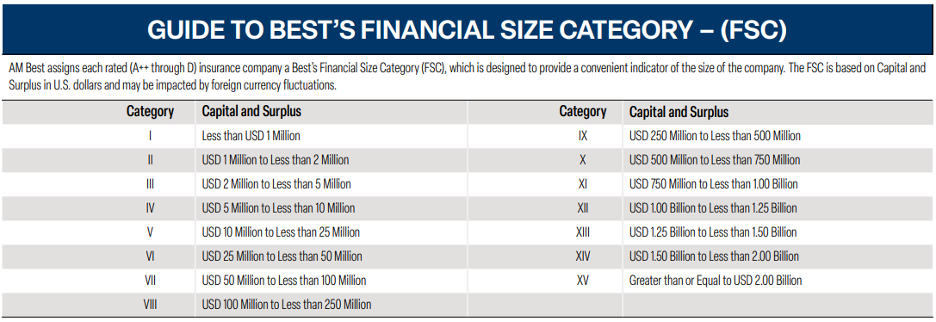

A.M. Best also categorizes the size of the insurance company’s policyholder surplus as seen in their Financial Size Category chart:

At Pearl Insurance, we rely on A.M. Best’s rating service when selecting our legal malpractice insurance offerings. We require a minimum Financial Strength Rating of A- (Excellent) and a minimum Financial Category of VIII ($100 million of policyholder surplus).

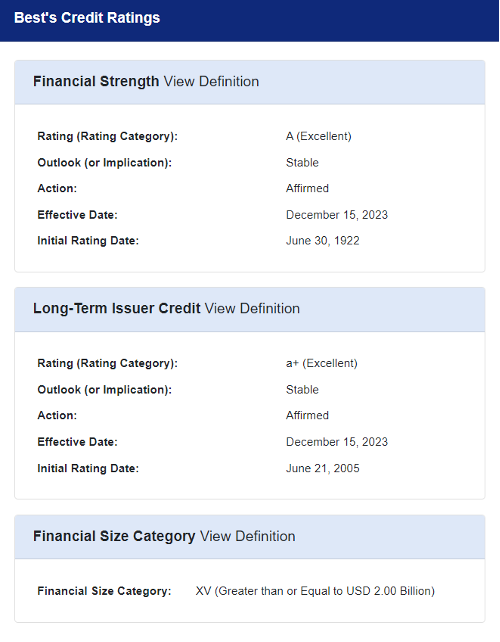

Rating Example

To give an example of an A.M. Best rating, here is their review of the Continental Insurance Company (CNA) as of August 2024.

What Should I Consider When Looking at Financial Strength Ratings?

It’s important to look at an insurance company’s current and past performances to confirm their financial stability, adequate size, and a stable trend.

Some red flags to watch for when considering your legal malpractice insurance carrier are:

- “NR” rating—indicating that the insurer has chosen not to be rated by A.M. Best or has been rating but asked for their rating to be withdrawn

- Financial Strength Ratings lower than A- (Excellent)

- A downward trend in their Financial Strength Rating

- A policyholder surplus less than $100 million

Given the extended time it can take to resolve a legal malpractice insurance claim, it is crucial to choose a financially stable carrier to ensure your defense and potential settlement costs will be covered. By looking at independent ratings, particularly from A.M. Best, and keeping an eye out for red flags, you can make informed decisions and secure reliable protection for your firm.

When you’re assessing professional liability insurance policies, be sure to consult with insurance experts, like Pearl Insurance. Our tailored approach and expertise in the legal realm can help guide you in selecting the most suitable coverage for your unique practice.

Questions?

At the end of the day, Pearl Insurance is here for you. We work tirelessly to help you find a policy that fits your firm’s exact needs. Pearl takes our responsibility to protect your firm seriously and will always put people before profit.

Want to know more? Find out for yourself.

(800) 346-6680 | pearlinsurance.com/professional-liability-insurance/

These highlights are intended to present a general overview for illustrative purposes only. It is not intended to constitute a binding contract. Please remember that only the relevant insurance policy issued to a law firm can provide the actual terms, coverages, amounts, conditions, and exclusions for an insured.

1“Insurance Company Ratings Explained.” Annuity Advantage, 2024.